Embedded finance video marketing 2026: Personalizing BNPL, Insurance, and Credit at Checkout with Invisible Payments

Key Takeaways

- Invisible payment explainer videos at checkout build trust and reduce friction while keeping users in flow.

- UPI Credit Line, BNPL, and embedded insurance must balance personalization with clear, compliant disclosures.

- Contextual micro-videos drive conversion and lower disputes by clarifying terms in under 20 seconds.

- Rule-based orchestration and tokenization enable automated, low-latency delivery of the right variant.

- API-first, white-label implementations plus measurement frameworks scale performance across partners.

Embedded finance video marketing 2026 is how Indian fintech and retail leaders will turn invisible payments and in-flow decisions into trust, conversion, and compliance. As the Indian digital economy matures, the friction between complex financial products and rapid checkout experiences has become the primary barrier to scale. By 2026, the convergence of UPI-led rails, sophisticated credit algorithms, and generative video technology will transform the point of sale from a mere transaction point into a high-conversion educational hub.

The Indian payments landscape is undergoing a seismic shift, with the total transaction value expected to reach approximately $10 trillion by 2026. This growth is underpinned by the National Payments Corporation of India (NPCI) launching the “Credit Line on UPI,” which allows for pre-sanctioned credit to be accessed instantly at the moment of purchase. Platforms like TrueFan AI enable enterprises to bridge the gap between technical eligibility and consumer comprehension by delivering personalized, real-time video explainers that clarify these complex financial offerings.

In this high-velocity environment, traditional text-based banners and static pop-ups are no longer sufficient. The 2026 trend emphasizes tokenization, AI-led actions, and “Embedded Finance 2.0,” where financial services are not just buttons but integrated ecosystems. Success now requires a seamless payment experience videos strategy that prioritizes transparency, regulatory adherence, and hyper-localization to capture the next 500 million Indian digital consumers.

Source: NPCI Credit Line on UPI

Source: PwC India Payments Report

Source: TCS 2026 Payments Trends

Source: NPCI Operating Circular (TeamLease RegTech)

1. The Rise of Invisible Payment Marketing Videos and Frictionless Payment Marketing

The concept of invisible payment marketing videos represents a paradigm shift in how financial products are sold within non-financial environments. In 2026, the goal is to eliminate the “interruption” phase of the payment journey, where a user is forced to navigate away from their cart to understand a loan’s terms or an insurance policy’s coverage. Instead, short, context-triggered explainers auto-play within the checkout screen, providing immediate clarity without disrupting the transaction flow.

Frictionless payment marketing is the strategic reduction of cognitive load through progressive disclosure. By using micro-videos that reveal information only when relevant—such as when a user hovers over a “Pay Later” option—brands can maintain high conversion rates while ensuring the user is fully informed. This is particularly critical for the UPI Credit Line at POS, where video clarifies limits, repayment dates, and dispute flows in under 20 seconds, satisfying both the user’s need for speed and the regulator’s need for transparency.

The technical foundation for these experiences lies in advanced tokenization and AI-led orchestration. As payment data becomes more secure and accessible, merchants can trigger seamless payment experience videos that are pre-populated with the user’s specific credit limit or EMI options. This level of integration ensures that the marketing is not a separate layer but a functional component of the payment architecture itself.

To execute this effectively, script design must prioritize “showing” over “telling.” Animated UI overlays can indicate exactly how a credit line is applied to a specific purchase, while localized voiceovers and captions ensure the message resonates across India’s diverse linguistic landscape. regional language video SEO. Legal statements should remain as on-screen supers with tap-to-expand drawers, ensuring that the primary video remains engaging while fulfilling all Reserve Bank of India (RBI) disclosure expectations.

Source: NPCI Product Overview

Source: TCS Insights on Tokenization

2. BNPL Integration Personalization and Point-of-Sale Credit Offers

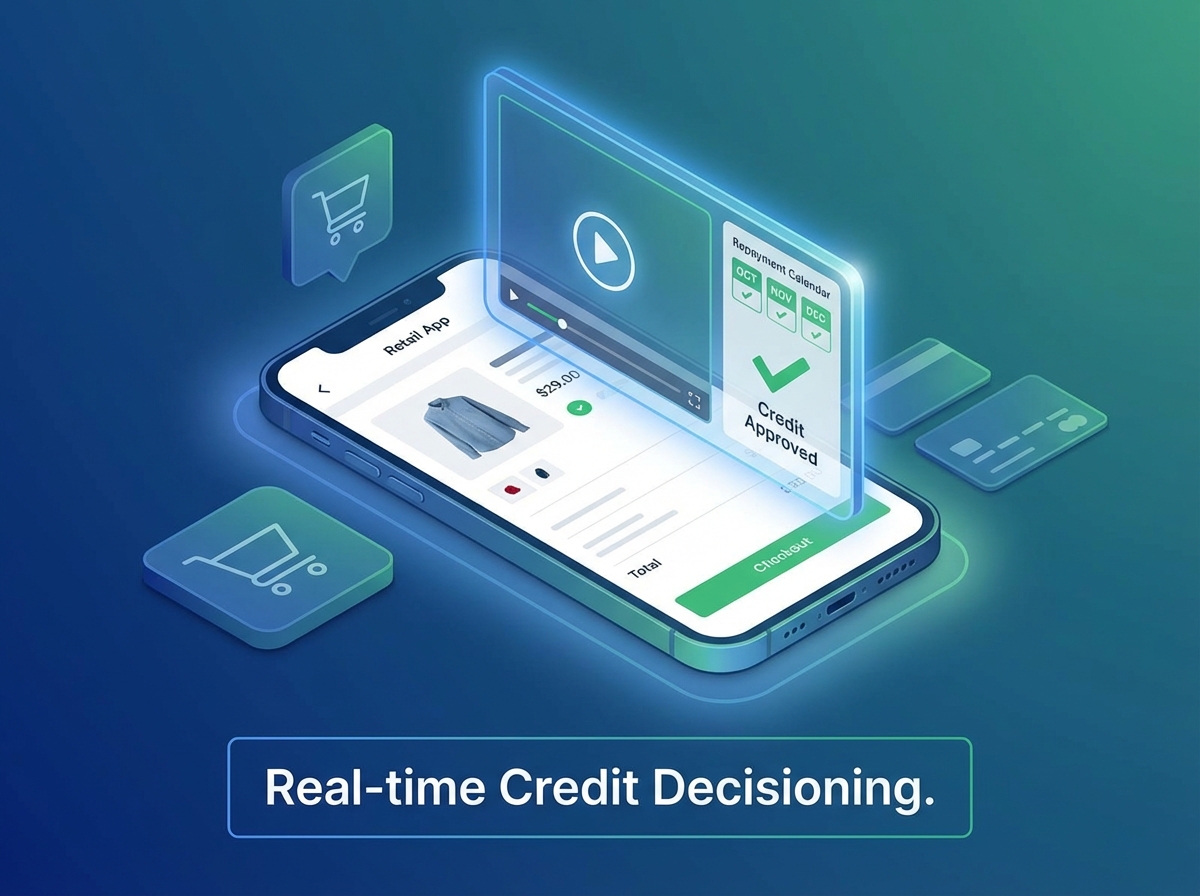

BNPL integration personalization has evolved from generic “Buy Now, Pay Later” buttons into sophisticated, data-driven video interventions. In 2026, the terms of a credit offer—including tenure, interest rates, and repayment schedules—are tailored in real-time based on the user’s cart value and repayment history. When a user selects a credit option, an instant credit decision video explains the outcome in plain language, visually mapping out the repayment calendar to prevent future defaults or disputes. BNPL payment collection automation.

Point-of-sale credit offers now leverage the “Credit Line on UPI” framework to provide bank-backed lending within merchant apps. This requires a delicate balance of marketing and compliance. The RBI’s Digital Lending Guidelines mandate clear disclosure of the Annual Percentage Rate (APR), fees, and grievance redressal mechanisms. Video content serves as the perfect medium for these disclosures, as it can present complex numerical data through intuitive visuals that are easier to digest than traditional fine print.

The orchestration of these videos follows a precise blueprint. Once a user triggers a credit-related event, the system must render a video variant—Approved, Alternate Offer, or Insufficient Data—in under 30 seconds. This low-latency delivery is essential to prevent drop-offs at the most sensitive stage of the funnel. By providing a “human” face to a credit decision through video, fintechs can build trust even when the news is a rejection or a counter-offer.

Key Performance Indicators (KPIs) for these campaigns have shifted from simple clicks to approval completion rates and watch-through metrics. Enterprises are finding that users who watch at least 70% of an instant credit decision video are significantly less likely to raise disputes later, as their understanding of the terms is fundamentally higher. BNPL default prevention campaigns. This alignment of marketing and customer success is the hallmark of embedded finance video marketing 2026.

Source: RBI Digital Lending Guidelines

Source: RBI FAQ on Lending

Source: Inc42 Digital Lending Playbooks

3. Embedded Insurance Video Campaigns with Contextual Finance Personalization

Embedded insurance video campaigns are revolutionizing how protection products are sold alongside core purchases. Whether it is accidental damage cover for a new smartphone or trip delay insurance for a flight booking, the 2026 approach uses contextual finance personalization to adapt the video’s message to the specific item in the cart. Instead of a generic insurance pitch, the user sees a 15-second video explaining exactly how the policy covers their specific product and how to initiate a claim.

In the electronics sector, for instance, a video can clarify the distinction between a manufacturer’s warranty and the add-on insurance being offered. By using first-party data like the product type and price, the video can dynamically update the premium cost and coverage limits shown on screen. This level of detail reduces the “buyer’s remorse” often associated with insurance and increases the attach-rate by making the value proposition undeniable.

Travel platforms are also seeing massive success with this model. When a user reaches the payment screen for a flight, a video can explain the Third-Party Administrator (TPA) process and the specific benefits of the trip delay cover based on their itinerary. This “just-in-time” education is far more effective than traditional email follow-ups, as it captures the user’s attention at the moment of highest intent.

Compliance remains a cornerstone of these campaigns. To satisfy IRDAI requirements, videos must include clear exclusions in the captions and provide a direct link to the full policy document. The user must provide affirmative consent—typically through a checkbox or a specific tap—before the insurance is bound. This ensures that the seamless payment experience videos are not just persuasive but also legally robust and ethically sound. insurance renewal automation.

Source: TCS 2026 Trends on AI-led Actions

Source: PwC India Innovation Report

4. In-App Financial Services Videos and Embedded Wallet Personalization

The lifecycle of a fintech user in 2026 is managed through in-app financial services videos that provide ongoing education and engagement. Beyond the initial transaction, these videos serve as “nudges” for credit line utilization, rewards redemption, and EMI management. By delivering these messages within the app’s feed or inbox, brands can maintain a continuous dialogue with the user, moving beyond a purely transactional relationship.

Embedded wallet personalization is a key component of this strategy. For users with digital wallets, videos can be used to encourage auto top-ups or to explain safe spending limits based on the user's cohort and recent activity. TrueFan AI's 175+ language support and Personalised Celebrity Videos allow these wallet nudges to be delivered in the user's native tongue, significantly increasing the likelihood of adoption in Tier 2 and Tier 3 cities. voice SEO in regional languages regional language voice shopping.

The onboarding phase is particularly critical. A 15-second “how your wallet works” video, with security tips and limit explanations, can reduce early-stage churn. As the user begins to use their credit line, contextual micro-videos can remind them of upcoming repayment dates and show them how to sync these dates with their calendar. This proactive approach to financial literacy builds long-term loyalty and reduces the risk of delinquency.

Retention campaigns also benefit from this personalized video approach. Milestone videos that celebrate a user’s “safe usage” or provide tips on maximizing rewards points create a positive feedback loop. In an era where UPI ubiquity has made basic payments a commodity, these personalized, value-added video experiences are the primary way for fintechs to differentiate themselves and maintain a high share of the user's wallet.

5. API Banking Video Campaigns and White-Label Finance Solutions Marketing

As the “Banking-as-a-Service” (BaaS) model matures in India, API banking video campaigns have become the standard for co-branded partner journeys. These campaigns allow banks and fintechs to insert personalized videos into a partner's app—such as a retail or gig economy platform—via simple webhooks. This ensures that the user receives a consistent, high-quality explanation of a credit offer or a KYC update, regardless of which platform they are currently using.

White-label finance solutions marketing enables enterprises to maintain brand continuity while leveraging the technical infrastructure of a financial partner. By using a library of templated videos that can be dynamically updated with the partner's logo, colors, and specific offer details, brands can scale their embedded finance offerings without a massive creative overhead. This is essential for large-scale co-lending partnerships, which are a major focus of India’s 2026 digital lending playbooks.

The implementation of these campaigns involves a sophisticated template system. Use cases like KYC updates, credit line upsells, and BNPL switches are pre-built and then customized via API at the moment of delivery. This allows for rapid experimentation; a brand can test different video variants across different partners to see which combination of tone, language, and offer structure yields the highest conversion lift.

Furthermore, the analytics for these campaigns are segmented by partner and cohort, providing deep insights into how different demographics interact with embedded lending marketing. This data-driven approach allows for the continuous optimization of the video content, ensuring that the white-label finance solutions marketing remains effective as market conditions and regulatory requirements evolve.

Source: Inc42 2026 Playbooks

Source: TCS Payments Trends 2026

6. Checkout Financing Automation and Regulatory Governance

Checkout financing automation is the engine that drives the delivery of the right video at the right time. By using rule-based orchestration, platforms can trigger specific video variants based on data attributes like cart value, user risk band, and tenure preference. For a high-value purchase, the system might trigger a “how EMI works” video that explicitly details the interest costs, whereas a returning user might see a shorter “renewal reminder” video for an expiring credit line.

This automation must be deeply integrated with regulatory governance. The RBI Digital Lending Guidelines are non-negotiable, requiring explicit consent for data access and the clear disclosure of all loan terms. Automated video flows must include “consent capture” moments where the user’s interaction with the video—such as watching it to completion or clicking a specific button—is logged for compliance purposes. This creates a robust audit trail that protects both the consumer and the lender.

The UPI Credit Line specifically requires that the issuing bank be clearly identified and that the repayment schedule be unambiguous. Checkout financing automation ensures that these details are dynamically inserted into the video based on the specific bank providing the credit. This level of precision is impossible to achieve with static content but is easily handled by modern video personalization engines that can render millions of unique variants on demand.

Accessibility and privacy are also paramount in 2026. Videos must have captions on by default and offer downloadable transcripts to ensure they are accessible to all users. Data minimization principles must be strictly followed, ensuring that only the necessary attributes are used to personalize the video. By combining frictionless payment marketing with rigorous governance, enterprises can build a sustainable embedded finance ecosystem that thrives in India’s complex regulatory environment.

Source: RBI Digital Lending FAQ

7. Enterprise Implementation Roadmap and Success Metrics

Implementing a comprehensive embedded finance video marketing 2026 strategy requires a structured approach to data, security, and scale. The first step is identifying the key trigger events within the checkout or app flow—such as a user selecting a specific payment option or reaching a cart value threshold. Once these triggers are mapped, the necessary attributes for contextual finance personalization, such as product type and risk band, must be integrated via APIs to enable real-time video rendering.

Solutions like TrueFan AI demonstrate ROI through their ability to handle millions of personalized variants with low-latency delivery. For an enterprise-grade rollout, security and compliance are the top priorities. This includes maintaining ISO 27001 and SOC 2 certifications and ensuring a consent-first model for all data and talent usage. Content moderation tools are also essential to prevent the dissemination of unapproved financial claims or misleading information.

Measurement and experimentation are the final pieces of the puzzle. Success should be tracked through a framework of core metrics, including conversion lift at checkout, approval completion rates, and the “attach-rate” for insurance or BNPL products. Experimentation should focus on variant testing—such as comparing “benefit-first” vs. “APR-first” video intros—and regional language optimization to find the most effective way to communicate with different user segments.

As you scale, the ability to perform “virtual reshoots” becomes a significant competitive advantage. This allows you to update regulatory copy or APR examples across thousands of videos instantly, without the need for new production shoots. By following this roadmap, Indian enterprises can lead the way in the next era of digital finance, turning every payment moment into an opportunity for engagement and growth.

Source: RBI Digital Lending Guidelines FAQ

Source: NPCI Credit Line on UPI

Source: PwC India Payments Report

Frequently Asked Questions

How do instant credit decision videos comply with RBI Digital Lending Guidelines?

Instant credit decision videos comply by incorporating the mandatory Key Fact Statement (KFS) details—such as APR, total interest, and repayment schedules—directly into the visual and audio narrative. They also feature tap-to-expand text drawers for full legal disclosures and require explicit user consent before proceeding, ensuring a transparent and compliant journey as per the latest RBI circulars.

What are the best practices for video disclosures in BNPL and POS credit?

Best practices include using clear, high-contrast captions, keeping legal statements on-screen for a minimum duration, and providing an easy-to-access “Terms and Conditions” link. The video should clearly state the name of the regulated entity (the bank or NBFC) providing the credit to avoid any ambiguity.

How fast can videos render and localize for India’s diverse languages?

With modern enterprise video engines, personalized videos can be rendered in under 30 seconds. These systems support over 175 languages, including major Indian regional languages, using high-fidelity lip-sync and voice retention to ensure the localization feels natural and trustworthy to the end-user. TrueFan AI provides this level of scale and speed for enterprise checkout flows.

How to handle data minimization and opt-outs in personalization?

Enterprises should only use the specific data points required for the personalization of the offer (e.g., name, cart value, and credit limit). Every video module should include a clear opt-out or “skip” option, and user consent for data usage should be refreshed whenever there is a significant change in the terms of service or the type of data being processed.

What is the expected conversion lift from using seamless payment experience videos?

While results vary by industry, enterprises often see a 15% to 25% increase in approval completion rates and a significant reduction in checkout abandonment. By replacing confusing text with clear, personalized video education, brands can resolve user doubts in real-time, leading to higher trust and better conversion outcomes.