Tax saving urgency marketing 2026: Enterprise BFSI playbooks to win before March 31

Estimated reading time: ~12 minutes

Key Takeaways

- Replace panic with orchestrated urgency using milestone-based cutoffs and transparent processing windows.

- Use behavioral nudges like loss aversion, scarcity, and social proof—paired with 1-click execution—to convert procrastinators.

- Deploy product-specific ELSS/NPS/Insurance playbooks that educate on T+2, 80CCD(1B), and 80D opportunities.

- Scale personalization with AI-driven videos and calculators while staying DPDP-compliant with granular consent.

- Segment for HNIs vs salaried employees to deliver white-glove advisory or instant value reveal experiences.

Tax saving urgency marketing 2026 is no longer about generic countdown timers; it is about precision-engineered behavioral interventions that respect the modern investor's cognitive load. As the March 31 fiscal deadline approaches, the Indian BFSI sector faces a unique convergence of regulatory shifts, digital-first consumer expectations, and the implementation of the DPDP Act. To capture the estimated 22% surge in last-minute tax-saving capital projected for the 2025–2026 cycle, enterprises must move beyond "panic" and toward "orchestrated urgency." This tax saving urgency marketing March 2026 strategy requires a sophisticated blend of fiscal planning urgency and behavioral nudge marketing to convert procrastinators into long-term wealth creators. Read the in-depth playbook on tax-saving panic marketing for March 2026.

The stakes for the 2026 fiscal year-end are unprecedented. With the increasing adoption of the New Tax Regime, the pool of taxpayers opting for Old Regime deductions (Section 80C, 80D, and 80CCD) has become more concentrated and value-conscious. For BFSI CMOs and Digital Heads, the objective is to operationalize ethical urgency across ELSS, NPS, and insurance portfolios. By leveraging data-driven insights and real-time processing windows, firms can mitigate the "deadline effect" while ensuring that money reaches Asset Management Companies (AMCs) and insurance providers before the final cutoff.

1. The 2026 Tax Urgency Landscape: India’s FY Cutoff and Urgency Anchors

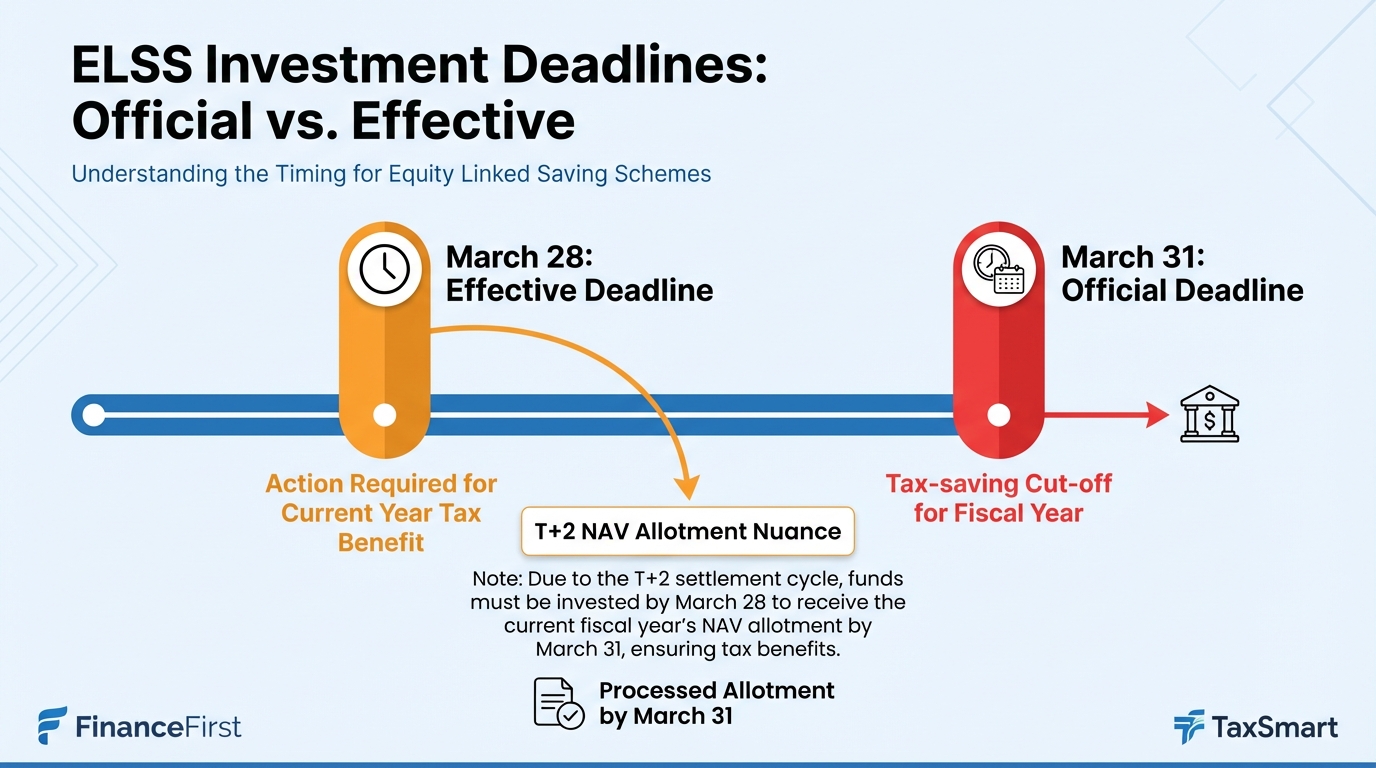

The Indian financial year ending March 31 serves as the ultimate hard stop for tax-saving actions. However, the operational reality is that the "effective" deadline often arrives much earlier. For instance, ELSS mutual fund panic campaigns must account for the T+2 NAV allotment nuance. If March 31 falls on a Monday, the effective deadline for allotment might be as early as March 27 or 28, depending on banking holidays and fund house cutoffs. Investors who wait until the final hours often find their funds unallocated for the current fiscal year, leading to missed tax benefits and significant customer dissatisfaction. Understand the March 31 investment rush dynamics and build a compliant countdown marketing plan.

In 2026, the urgency is further amplified by the Section 80CCD(1B) additional deduction. This provision allows for an extra ₹50,000 tax deduction specifically for NPS Tier I contributions, over and above the ₹1.5 lakh limit of Section 80C. Marketing playbooks must emphasize this "exclusive" window, as many taxpayers overlook this additional saving opportunity until the final weeks of March. Similarly, insurance tax benefit automation is critical for Section 80D health insurance premiums, where senior citizen parents' coverage can offer enhanced limits that remain underutilized.

The "March 31 checklist" has become a cultural touchstone for Indian savers. From reconciling payroll proofs to finalizing investment declarations, the final quarter of the year is characterized by high intent but also high friction. Enterprise strategies must focus on reducing this friction through automated document workflows and clear, time-sensitive communication. By framing the deadline not just as a date, but as a series of operational milestones (e.g., "Last day for e-mandate setup," "Final window for physical branch deposits"), BFSI players can guide users through the funnel with professional authority.

Sources:

2. Behavioral Nudge Marketing: The Psychology of March 31

To drive conversion during the tax season, BFSI enterprises must master behavioral nudge marketing. This involves using psychological triggers to influence decision-making without restricting choice. The most potent trigger in this context is loss aversion. Research indicates that the pain of losing ₹46,800 (the maximum tax saving for an individual in the 30% bracket under 80C) is far more motivating than the joy of gaining the same amount. Reframing marketing copy from "Save tax now" to "Don't leave ₹46,800 unclaimed" significantly increases engagement rates. Explore cognitive bias tactics for ELSS marketing.

The "deadline effect" or scarcity is another critical lever. As the March 31 cutoff nears, the perceived value of the investment opportunity increases. However, this must be balanced with social proof. By displaying anonymized, cohort-based data—such as "85% of salaried professionals in your bracket have completed their 80C declarations this week"—enterprises can trigger a healthy sense of FOMO (Fear Of Missing Out). This validates the user's intent and reduces the "present bias," where individuals prioritize immediate consumption over future tax savings.

Ethical execution is paramount. Urgency should never devolve into misinformation. Every nudge must be accompanied by clear disclosures regarding product risks, such as the 3-year lock-in for ELSS or the annuity requirements for NPS. Choice overload is a common pitfall; instead of presenting twenty different mutual funds, the UX should offer 3-option "good/better/best" packs tailored to the user's salary and risk profile. This reduction in friction, combined with 1-click execution paths, ensures that the behavioral triggers lead to actual financial outcomes rather than analysis paralysis.

3. High-Conversion Enterprise Playbooks for ELSS, NPS, and Insurance

The core of a successful tax saving urgency marketing 2026 strategy lies in product-specific playbooks. For ELSS mutual fund panic campaigns, the focus must be on the "last-window" orchestration. This involves a sequenced communication plan: D-7 (Plan your allocation), D-4 (Processing time alert), and D-1 (Final NAV cutoff). Given the T+2 allotment rules, the campaign must educate the user that "Investing on March 31 might be too late." This transparency builds long-term trust while driving earlier action. See the March 31 investment rush checklist.

NPS enrollment deadline videos should specifically target the Tier I account for the Section 80CCD(1B) benefit. These videos should be short (under 60 seconds) and address the common confusion between Tier I (tax-deductible) and Tier II (flexible withdrawal) accounts. By using dynamic overlays that show the user's specific tax-saving potential based on their income bracket, these videos transform a complex pension product into a simple, immediate tax-saving tool. For corporate employees, highlighting the Section 80CCD(2) employer contribution can further sweeten the deal. See NPS enrollment deadline video tactics and learn about NPS personalization strategies.

Insurance tax benefit automation represents the next frontier in BFSI retention. By auto-detecting premium gaps compared to the previous year and identifying upcoming renewal windows, enterprises can send personalized nudges for 80C and 80D compliance. For example, if a user has not utilized their ₹25,000 limit for health insurance under Section 80D, the system can trigger a bilingual video reminder suggesting a top-up or a policy for senior citizen parents (which offers an additional ₹50,000 limit). This level of personalization ensures that the marketing feels like a service rather than a sales pitch.

Sources:

4. Segmented Urgency: HNI and Corporate Employee Tax Planning

A one-size-fits-all approach fails in the high-stakes environment of March. HNI wealth management urgency requires a "white-glove" digital experience. For this segment, the focus shifts from simple 80C products to complex tax harvesting, NPS employer carve-outs, and multi-asset model portfolios. Financial advisory video consultations are the primary conversion tool here. By embedding a 2-click scheduler within a personalized video invite from their Relationship Manager (RM), HNIs can receive bespoke advice on optimizing their tax liability across family accounts before the deadline.

Corporate employee tax planning requires a different set of tools, specifically 80C investment personalized calculators. These calculators should be embedded within HR co-branded microsites, pulling real-time data from payroll systems to show exactly how much "tax is left on the table." If an employee has only declared ₹1.1 lakh of their ₹1.5 lakh 80C limit, the calculator should immediately suggest ELSS or insurance products to bridge the ₹40,000 gap. This "instant value reveal" is the most effective way to drive volume in the salaried segment. See 80C personalized video use cases and explore tax-saving ROI calculators.

Salary-specific investment videos further enhance this strategy by tailoring the narrative to the user's career stage. An entry-level employee might receive a video focused on the simplicity of ELSS and the low entry barrier of NPS, while a mid-career professional receives content focused on 80D health covers for their growing family. These videos, delivered via WhatsApp and in-app banners, ensure that the fiscal planning urgency is relevant to the individual's life stage, significantly increasing the likelihood of a last-minute conversion.

5. Compliance, DPDP Act, and Ethical Urgency

In 2026, every tax saving urgency marketing 2026 campaign must be built on a foundation of data privacy. The Digital Personal Data Protection (DPDP) Act 2023 mandates that consent for data processing must be "freely given, specific, informed, and unambiguous." For BFSI enterprises, this means that every "tax-saving nudge" must be backed by a clear consent log. Consent UI blocks must be granular, allowing users to opt-in specifically for "tax-saving recommendations" or "advisory callbacks" across different channels like WhatsApp, SMS, and Email. Learn how to capture consent via interactive video journeys and see DPDP-compliant personalization strategies.

Ethical urgency also demands financial suitability. Marketing materials must clearly state the risks and limitations of each product. ELSS campaigns must prominently display the 3-year lock-in period, and NPS content must explain the annuity requirements upon retirement. By integrating these disclosures into the user journey—rather than hiding them in the fine print—enterprises demonstrate authoritativeness and trustworthiness. This approach not only ensures regulatory compliance with SEBI and IRDAI but also reduces the risk of post-purchase dissonance and complaints.

The implementation of "Consent Managers" as per the MeitY framework will be a standard requirement by 2026. These platforms allow users to manage, withdraw, and track their consents in real-time. BFSI firms that proactively adopt these transparency standards will gain a significant competitive advantage. By framing data protection as a core part of the customer's financial security, brands can turn a regulatory hurdle into a trust-building opportunity during the high-pressure tax season.

Sources:

6. Scaling Personalization with TrueFan AI

Executing a hyper-personalized tax season strategy at the scale of millions of customers requires advanced AI orchestration. Platforms like TrueFan AI enable BFSI enterprises to generate one-to-one video communications that address each customer by name, salary bracket, and specific tax gap. Instead of a generic "Save Tax" email, a customer receives a 30-second video explaining exactly how they can save ₹15,000 by investing in NPS before the March 31 deadline. This level of precision is what defines the next generation of tax saving urgency marketing 2026. See how 80C personalized videos drive action.

TrueFan AI's 175+ language support and Personalised Celebrity Videos allow brands to reach customers in their preferred regional language, which is critical for penetration in Tier-2 and Tier-3 cities. The ability to perform "virtual reshoots"—updating countdown timers and offer lines in real-time without new production—allows marketing teams to iterate daily during the final 12-day surge. For example, a video sent on March 25 can automatically update its "Days Left" overlay every time it is opened, maintaining the psychological pressure of the deadline. Measure impact with tax-saving ROI calculators.

Solutions like TrueFan AI demonstrate ROI through significantly higher engagement and conversion rates compared to static assets. By integrating these AI-driven videos with 80C investment personalized calculators and CRM data, BFSI firms can create a seamless, automated funnel. From the initial nudge to the final e-KYC and payment, the journey is guided by a consistent, personalized voice. This not only drives immediate AUM growth but also sets the stage for BFSI retention tax season strategies, where lump-sum tax savers are converted into long-term SIP investors in the following quarter.

7. Conclusion & FAQ

The success of tax saving urgency marketing 2026 hinges on the ability of BFSI enterprises to balance aggressive conversion goals with ethical, data-driven personalization. By mapping behavioral nudges to specific product playbooks—ELSS, NPS, and Insurance—and delivering them through high-impact channels like personalized video, firms can turn the March 31 deadline into a predictable revenue engine. The integration of DPDP-compliant consent frameworks and AI-powered scaling ensures that this urgency is both sustainable and brand-safe. As the fiscal year closes, the winners will be those who reduce the customer's cognitive load while maximizing their financial outcomes.

Recommended Internal Links

- Tax-saving panic marketing: March 2026 strategy guide

- Managing the March 31 investment rush

- March 31 countdown marketing 2026

- Cognitive bias techniques for ELSS marketing

- NPS enrollment deadline videos

- Personalizing NPS enrollment nudges

- 80C investment personalized videos

- Tax-saving ROI calculators

- Interactive video data capture

- DPDP-compliant personalization strategies

Frequently Asked Questions

What is the effective deadline for ELSS investments in March 2026?

While the official deadline is March 31, the effective deadline for ELSS is often March 28 or earlier due to the T+2 NAV allotment rule. To claim Section 80C benefits for the current fiscal year, the funds must be realized by the AMC and units must be allotted before the cutoff. Always check for banking holidays in the final week of March. Learn more about effective ELSS cutoffs.

Can I claim the ₹50,000 NPS deduction over and above the ₹1.5 lakh 80C limit?

Yes. Under Section 80CCD(1B), individuals can claim an additional deduction of up to ₹50,000 for contributions to the NPS Tier I account. This is independent of the ₹1.5 lakh limit under Section 80C. See how to communicate 80CCD(1B) via personalized videos.

How does the DPDP Act affect tax-saving marketing on WhatsApp?

Under the DPDP Act 2023, BFSI firms must obtain explicit, informed, and purpose-bound consent before sending marketing messages on WhatsApp. Users must be able to withdraw consent easily, and all consent events should be logged for audits. Discover consent capture best practices.

Is health insurance premium for parents eligible for tax savings?

Yes. Under Section 80D, you can claim a deduction for premiums paid for yourself, spouse, and children, plus a separate deduction for parents. If parents are senior citizens (60+), the limit is ₹50,000, creating a significant tax-saving opportunity.

What happens if I miss the March 31 deadline for tax-saving investments?

If you miss the March 31 deadline, you cannot claim those investments as deductions for the 2025–26 financial year and must pay tax per your slab. This is why early action and milestone-based planning are critical.